STRATEGIC OVERVIEW

Practitioner breakdown of The CFO OS: Restructuring Corporate Close, Audit, and Cash Reconciliation Loops — written for CTOs, VP Engineering, and India GCC leads shipping production AI with measurable ROI.

By Vatsal Shah | 2026-07-13 | 22 min read

Table of Contents

- Introduction

- What is the CFO OS?

- Why the CFO OS Matters in 2026

- The Monthly Close Failure: Why Periodic Accounting Hinders Agility

- Continuous Cash Reconciliation: Real-Time Cash Flow Analysis at the Edge

- Autonomous Ledger Auditing: Designing Parser Agents for Discrepancy Checks

- Predictive Liquidity: Modeling Mid-Term Operational Working Capital Needs

- Legacy Periodic vs. Autonomous CFO OS

- Pitfalls and Modern Anti-Patterns

- Anti-Pattern 1: Webhook Ingestion Without Event Validation and Idempotency

- Anti-Pattern 2: Alert Fatigue from Zero-Variance Match Rigidness

- Anti-Pattern 3: Stale FX Reference Data on International Cross-Border Ledger Reconciliation

- Anti-Pattern 4: Balance Sheet Pooling Without Inter-Company Entity Segregation

- Futuristic Horizon: 2027–2030 Roadmap

- Key Takeaways

- What to Do Monday Morning

- FAQ

- About the Author

Introduction

The traditional corporate finance department operates on a broken temporal model. For decades, the "monthly close" has been treated as an immutable law of business. Every 30 days, finance teams scramble to gather bank statements, reconcile ledger accounts, match invoices, and compile reports. This periodic sprint results in a retrospective view of corporate health that is often 15 days out of date by the time it reaches leadership. In the fast-moving business landscape of 2026, relying on a retrospective close is like steering a high-speed vehicle by looking exclusively in the rearview mirror.

Waiting for the end of the month to understand cash positioning, liquidity trends, and general ledger reconciliation introduces severe operating liabilities. In an era where cloud compute costs shift by the minute, supply chains adjust dynamically, and capital markets demand instant agility, retrospective accounting is a critical bottleneck. The modern enterprise requires a continuous financial visibility posture that turns accounting from a batch-oriented back-office function into a real-time corporate operating system.

The solution lies in restructuring the corporate close from a periodic manual bottleneck into a continuous, automated stream. This article details the transition to the CFO Operating System (CFO OS)—an autonomous corporate finance architecture that leverages streaming data ingestion, discrepancy parser agents, and predictive liquidity models to deliver a continuous, real-time audit posture. We will examine how this system interfaces with transactional banking feeds, manages ledger alignment automatically, and utilizes probabilistic capital forecasting to optimize treasury yields.

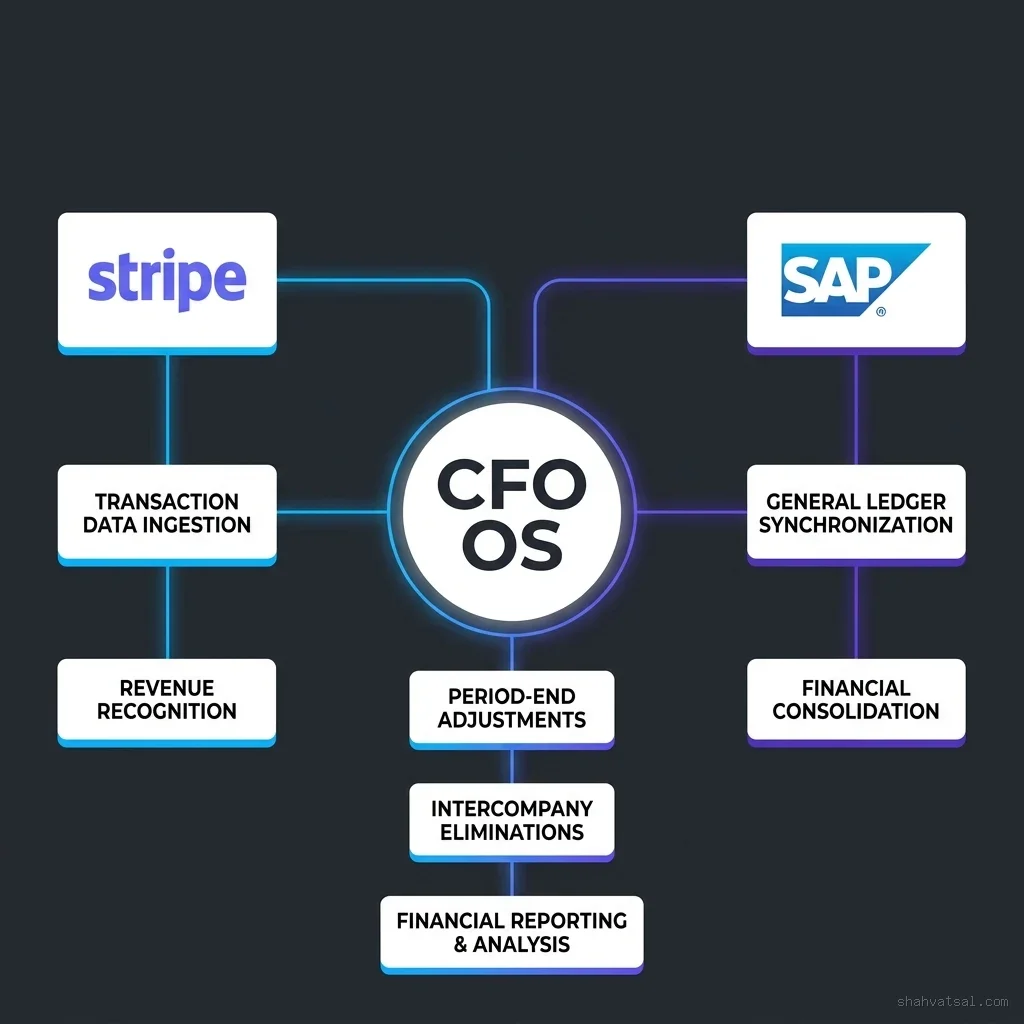

What is the CFO OS?

The CFO OS is defined as a unified corporate finance software layer that shifts accounting from batch processing to continuous processing. Instead of treating ledger entries as static items to be checked at month-end, the CFO OS treats every transaction as a real-time event that must be ingested, normalized, reconciled, and audited within minutes of occurrence. This structural shift requires replacing file-based exports with streaming database triggers and direct application programming interface (API) connections.

In a traditional setup, accounting systems remain passive until accountants import files. The CFO OS, by contrast, operates actively. It relies on direct integrations with bank API endpoints, payment gateways, credit facilities, invoice management software, and enterprise resource planning (ERP) systems. By utilizing continuous cash reconciliation loops and autonomous matching logic, the system aligns ledger balances against cash positions dynamically throughout the day.

This real-time alignment creates a single source of truth for the entire organization. Treasury departments can view exact cash allocations, operational managers can track project budget burns instantly, and tax teams can monitor localized liability build-ups in real time. Rather than relying on human accountants to spot ledger variances, the CFO OS uses stateful software agents to verify balance sheets continuously, flagging discrepancies the moment they cross settlement gateways.

Architectural Blueprint: Edge Microservices for Financial Processing

To achieve this level of operational concurrency, the CFO OS is structured as a distributed network of edge microservices. Instead of a monolithic ERP server processing batch jobs overnight, the architecture partitions financial tasks into dedicated service blocks. Each block runs independently on edge infrastructure, ensuring minimal latency and high availability.

The core service blocks include:

- Ingestion Edge Nodes: These services are deployed close to the transactional gateways. They maintain persistent connections to bank APIs and payment systems, listening for webhook events and parsing raw payloads into normalized message queues.

- Matching Microservices: These nodes subscribe to normalized transaction streams and reference data caches (such as invoice registries and purchase orders). They execute matching algorithms and update transaction status flags.

- Audit Checkpoint Validators: These services run continuous integrity checks across ledger tables, ensuring that double-entry rules are maintained and that total asset values correspond to bank balances.

- Liquidity Forecasting Engines: These background services pull verified transaction streams and run probabilistic mathematical models to project operational runway and capital needs.

By segregating these tasks, the enterprise ensures that transaction spikes in customer payments do not impact internal general ledger performance. Furthermore, if a bank API goes offline, the Ingestion Edge Node queue caches the incoming webhooks, resuming parsing immediately when the connection is restored, ensuring zero data loss.

Interfacing Protocols: Transitioning from MT940 to ISO 20022 and JSON Webhooks

For decades, bank statement data was transmitted using legacy flat-file formats like Swift MT940 or BAI2. These files are typically exported at the end of the day or week and contain unstructured text strings in their memo fields. Parsing MT940 files requires complex regex scripts that frequently break due to minor alterations in bank formatting, necessitating manual intervention by finance clerks.

The CFO OS transitions the enterprise to modern interfacing protocols:

- ISO 20022 XML Messages: Unlike MT940, the ISO 20022 standard represents financial messages (like CAMT.053 statement logs) in structured XML. Every element—including bank charges, transactional timestamps, exchange rates, and counterparty entities—has a dedicated, standard XML tag. This structured format allows edge parsers to read financial data with complete accuracy.

- Real-Time JSON Webhooks: For immediate transaction visibility, the system uses bank API webhooks. Modern financial institutions push JSON payloads directly to corporate endpoints the second a payment clears. The payload contains transaction IDs, settled amounts, currency codes, and descriptive strings, enabling sub-second ledger updates.

By utilizing ISO 20022 and JSON webhooks, the financial automation pipeline eliminates the need for unstructured text scraping, ensuring that transaction ingestion is both robust and real-time.

Why the CFO OS Matters in 2026

The enterprise operating model has evolved. The rise of multi-cloud architectures, real-time billing, API-driven vendor networks, and globally distributed payment gateways has dramatically increased transaction velocity. In 2026, corporate treasurers must manage capital allocation across multiple jurisdictions, currencies, and yield curves simultaneously. Wait-times associated with manual reconciliation loops are no longer just administrative bottlenecks—they represent significant capital inefficiencies.

[ ERP Systems ] ---------\

[ Bank API Feeds ] -------> [ Streaming Ingestion ] ---> [ Continuous Reconciliation Engine ]

[ Payment Gateways ] ----/Furthermore, traditional audits are slow and expensive. When auditors discover discrepancies weeks or months after the fact, tracing the root cause requires substantial forensic labor. By introducing continuous ledger reconciliation and automated anomaly detection, enterprises reduce audit readiness time from weeks to zero, mitigate operational fraud instantly, and avoid liquidity crunches by maintaining optimized, predictive working capital reserves.

In the context of modern technology stacks, the CFO OS bridges the gap between software execution and financial record-keeping. As businesses adopt autonomous agents to run operational workflows, the underlying financial ledger must keep pace. A continuous reconciliation stack ensures that as software processes micro-payments, routes API charges, or purchases edge compute resources, the financial impacts are written, balanced, and verified immediately.

The Unit Economics Crisis in the Era of High-Frequency SaaS and GenAI Services

Modern enterprises are consuming API services, cloud computing infrastructure, and generative AI models at unprecedented volumes. In 2026, standard billing models have transitioned from fixed annual contracts to high-frequency consumption-based pricing. Companies are charged per token consumed, per CPU-hour utilized, or per API request resolved.

This transaction granularity introduces a unit economics crisis for traditional accounting teams. If an enterprise uses thousands of distributed AI models across different business units, the monthly invoice can contain millions of micro-line items. Reconciling these bills manually at the end of the month is physically impossible, leading to a complete lack of control over cloud spend.

The CFO OS addresses this crisis by integrating FinOps transformation data directly into the corporate general ledger. When an edge compute node runs a query, the cost is registered in a local ingestion channel, allowing the system to match utility billing data continuously. If a specific business unit experiences a budget run-away due to an unoptimized AI loop, the CFO OS flags the cost spike in real time, letting management terminate the process before a massive liability accumulates.

Mitigating Intra-Day Counterparty Credit Risk

With the acceleration of global commerce, enterprises are frequently exposed to intra-day counterparty credit risk. When a company fulfills a high-value order based on an unverified payment confirmation, it assumes the risk that the transaction may fail during settlement clearing loops. In legacy accounting setups, verification occurs long after fulfillment, leaving the enterprise vulnerable to fraudulent chargebacks or bank reversals.

By implementing continuous reconciliation loops, the CFO OS mitigates this risk. As soon as a transaction clears the bank network, the system parses the cryptographic settlement confirmation and updates the client's credit ledger immediately. The operational fulfillment system queries this ledger via API before shipping, ensuring that high-value assets are only released when settlement is cryptographically verified, minimizing default rates.

The Monthly Close Failure: Why Periodic Accounting Hinders Agility

The periodic manual close is a legacy of paper-based accounting systems. The process is defined by a sequential workflow that accumulates stress at the end of every fiscal period. This workflow traditionally follows a strict, step-by-step path:

- Transaction Accumulation: Sales, purchases, journal entries, and bank clearings accumulate silently over 30 days, creating a massive backlog of unverified data.

- Reconciling Statements: Accountants log into bank portals, download CSV or PDF statements, and attempt to align bank records with internal ledger accounts.

- Adjusting Ledgers: Ledger entries are posted post-facto to account for bank fees, interest payments, bad debt write-offs, depreciation, and foreign exchange variances.

- Consolidation: Financial results from subsidiary entities are rolled up into consolidated corporate parent records, requiring complex currency translations and inter-company elimination entries.

- Reporting & Auditing: Statements of cash flows, balance sheets, and income statements are generated, reviewed by internal controllers, and prepared for external audit review.

Citation Anchor: Enterprise Close Latency Metrics

A 2025 financial benchmarks report by APQC indicates that top-performing finance organizations require an average of 4.8 days to close their monthly books, while bottom-performing organizations require 10 or more days. This delay means strategic planning decisions made in the first week of a month are based on operational realities from six weeks prior, directly impacting enterprise capital deployment efficiency.

This batch approach introduces significant liabilities. First, processing delays prevent timely detection of duplicate billing, billing leaks, and vendor overcharges. If a supplier overbills an enterprise on the second day of the month, a periodic accounting team will not detect the variance until the close process begins in the following month. By then, the invoice has been paid, the funds have left the corporate accounts, and reclaiming the capital requires a protracted dispute process.

Second, the heavy workload at month-end causes staff burnout, increasing the probability of clerical errors. Under close-week pressure, accountants are forced to rush through complex allocations, ledger adjustments, and matching exceptions, leading to reporting inaccuracies that must be resolved in subsequent quarters.

Finally, the retrospective nature of the reports makes it impossible to dynamically redirect funds to maximize yield or support short-term operational expenses. If corporate cash reserves are tied up in low-yield accounts because the treasury team lacks real-time visibility into consolidated cash positioning, the enterprise is effectively losing money due to idle capital.

Legacy Closing Loops: The Core Stress Points Analyzed

To understand why the manual close fails, we must analyze the specific points of failure in the ledger synchronization cycle:

- The Invoicing Mismatch: Standard billing systems register revenue when an invoice is issued, while banking gateways register cash when payment is settled. If a customer settles an invoice on the last day of the month but the bank clears it on the first day of the next month, a manual accountant must post an "in-transit cash" entry, consuming hours of manual adjustment.

- The Adjustment Backlog: Bank charges, FX spreads, and transaction gateway transaction fees are typically debited directly from bank balances. These charges do not appear in purchase orders, meaning accountants must manually match and write adjustment logs for thousands of tiny fee deviations.

- The Inter-company Gridlock: In global organizations, subsidiaries frequently buy and sell services from each other. At month-end, these intercompany balances must net to zero. If one entity registers an expense in a different currency than its parent registers the revenue, the entire consolidation gridlocks until the exchange rates are manually matched and corrected.

The Deferred Revenue Reconciliation Challenge

For subscription-based SaaS businesses, revenue recognition is highly complex. Under accounting standards like ASC 606 / IFRS 15, revenue from a contract must be recognized as the performance obligation is satisfied over time, rather than when the cash is collected. This requires companies to maintain complex deferred revenue schedules.

In a periodic close model, adjusting deferred revenue accounts requires compiling billing spreadsheets and running amortization calculations at the end of the month. If a client upgrades, downgrades, or cancels their subscription mid-month, accountants must recalculate the schedule manually. This introduces severe lag and errors in reporting monthly recurring revenue (MRR).

The CFO OS automates this calculation. The system tracks subscription events continuously via billing system webhooks. As obligations are fulfilled (e.g. on a daily basis), the matching microservice automatically shifts the appropriate balance from the deferred revenue liability account to the recognized revenue asset account. This continuous amortization provides controllers with up-to-the-minute revenue metrics, eliminating month-end adjustments.

Consolidation Latency in Multi-Jurisdictional Corporate Group Structures

For international corporations, consolidating books across different regions is a major bottleneck. Each subsidiary operates in its local currency, using its local chart of accounts, and complies with local tax laws. To compile corporate reports, the parent company must translate every asset, liability, revenue, and expense entry into a single base currency, using appropriate exchange rates for the translation date.

In traditional models, this translation occurs during the consolidation phase of the monthly close. If a subsidiary in Germany has not finished its local close, the parent company in the US cannot complete corporate consolidation. A delay in one region stalls reporting globally.

The CFO OS eliminates this dependency through continuous translation pipelines. Every transaction posted to a local subsidiary ledger is instantly copied, translated to the base currency using the real-time FX rate for that second, and written to a mirror corporate consolidation ledger. This parallel processing allows corporate management to view consolidated, currency-adjusted financial reports at any point during the month, completely removing consolidation latency.

Continuous Cash Reconciliation: Real-Time Cash Flow Analysis at the Edge

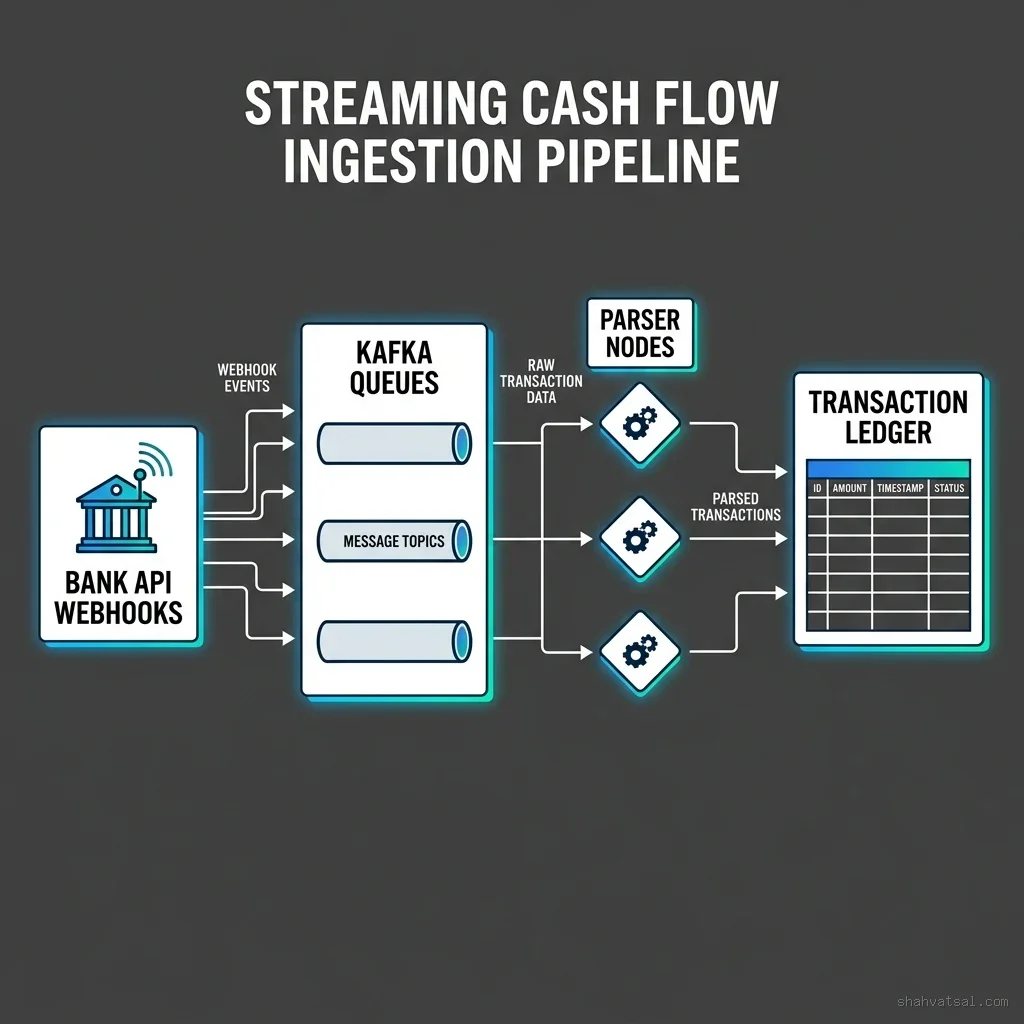

To eliminate the monthly close bottleneck, companies must deploy a streaming reconciliation model. Continuous cash reconciliation loop patterns replace daily or weekly bank files (like MT940 or BAI2) with Webhook-driven bank API endpoints (such as those provided by modern platforms like Plaid, Stripe, or direct corporate APIs from JPMorgan Chase and HSBC).

When a cash transaction occurs, the transaction payload is pushed instantly to a central financial ingestion pipeline.

The ingestion pipeline handles:

- Normalization: Standardizing JSON payloads from different bank APIs into a single transaction schema.

- Deduplication: Utilizing idempotent request IDs to prevent duplicate entries from network retries.

- Categorization: Running transaction descriptions through matching patterns to link them to corresponding purchase orders or billing records.

For example, when a vendor payment clears, the webhook fires, the system matches the transaction hash with an open Accounts Payable entry, updates the general ledger cache, and adjusts cash position models immediately. The cash ledger is updated in real time, transforming the balance sheet into a live data feed.

This streaming ingestion architecture relies on message broker queues (such as Apache Kafka or RabbitMQ) to handle peak transaction loads. If a company processes thousands of payments per minute, the queue absorbs the incoming webhook payloads, distributes them across parsing nodes, and guarantees that each transaction is processed, matched, and committed sequentially. This prevents write conflicts and database deadlocks that often occur when legacy ERP systems are subjected to high-frequency transaction updates.

Furthermore, continuous reconciliation at the edge utilizes the ISO 20022 messaging standard. This XML-based schema embeds rich transactional metadata directly into the payment message, including invoice numbers, purchase order IDs, tax structures, and counterparty details. By standardizing on ISO 20022, the ingestion pipeline can read this structured metadata directly, eliminating the need for complex, error-prone regex matching against unstructured bank memo strings.

Building the Ingestion Engine: Kafka Queues, Idempotency Checks, and Data Deduplication

At scale, the cash ingestion engine must guarantee that every transactional message is processed exactly once. If a network disruption causes a bank API to retry a webhook delivery, the pipeline must identify and reject the duplicate payload to avoid corrupting ledger balances.

This reliability is achieved using an idempotent database architecture combined with distributed streaming queues:

- Ingestion Edge Nodes receive the JSON payload from the bank webhook.

- The node extracts the bank's unique transaction hash (e.g.

bank_txn_id) and places the message in an Apache Kafka topic. - Consumer Workers retrieve the message from the queue and attempt to write a transaction record to an operational ledger database using a unique constraint on the

bank_txn_idcolumn. - If the database throws a key violation exception, the transaction is recognized as a duplicate and silently discarded.

- If the write succeeds, the ledger state is updated and the message is passed to the matching engine.

By enforcing database-level unique constraints, the ingestion engine guarantees complete ledger consistency, even during volatile network conditions or unexpected API retry storms.

Heuristic Matching Framework: Rules for Invoice and Purchase Order Binding

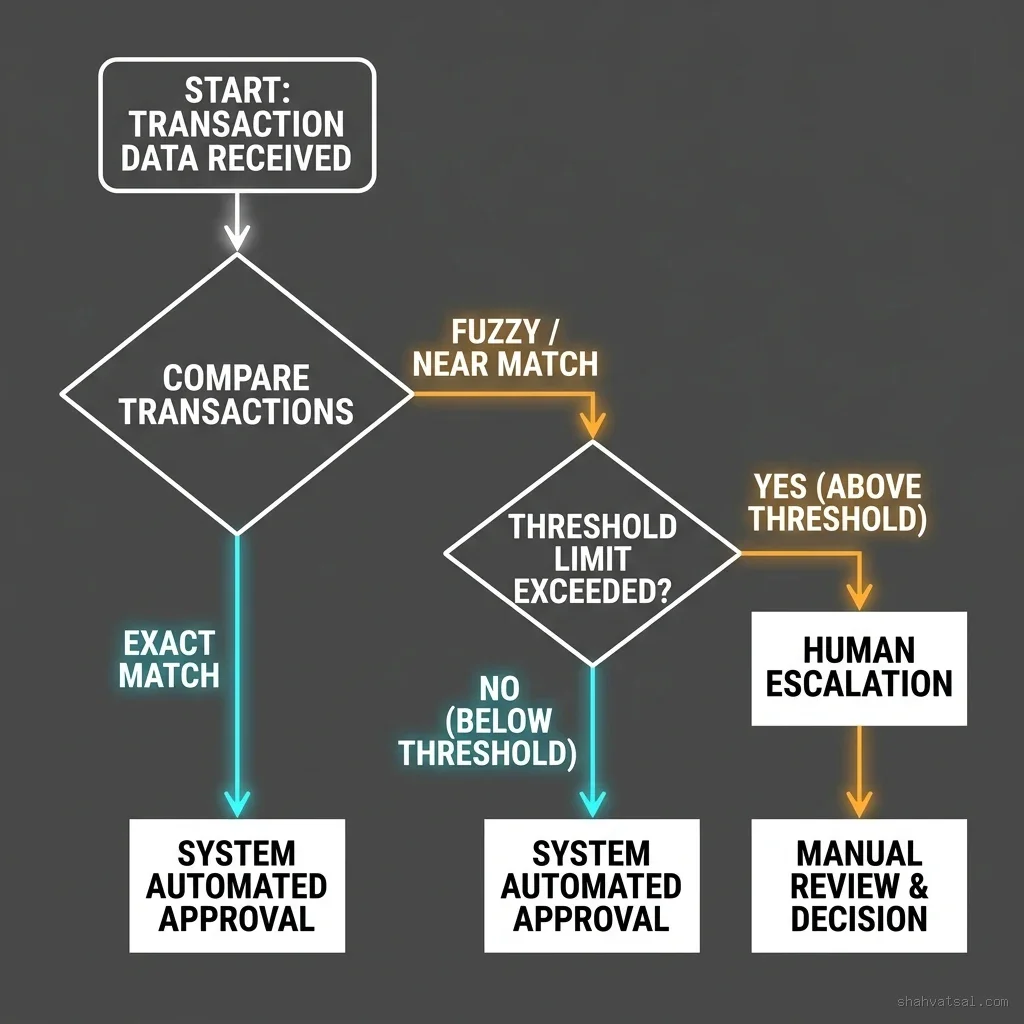

Once a transaction is safely written to the ledger, it must be matched to corresponding invoices or purchase orders. The CFO OS uses a heuristic matching framework that classifies matches by confidence scores:

- Exact Match (Confidence: 100%): The transaction payload contains a structured reference ID (such as an ISO 20022 invoice code) that matches an outstanding invoice ID exactly, and the settled cash amount matches the expected balance.

- Metadata Fuzzy Match (Confidence: 80%–95%): The transaction memo lacks an invoice ID, but the counterparty name, transaction date, and payment value correspond closely to an open purchase order within acceptable tolerances.

- Dynamic Threshold Match (Confidence: 60%–80%): The payment matches an invoice value, but has minor fee differences (e.g. transaction charges or wire fees) that fall within threshold limits.

When a confidence score exceeds the automated matching threshold (e.g. 90%), the system settles the invoice, marks the general ledger account reconciled, and updates cash models. If the match falls below the threshold, the parser agent initiates an exception resolution path, preventing unverified transactions from automatically modifying ledger records.

Autonomous Ledger Auditing: Designing Parser Agents for Discrepancy Checks

Even with real-time ingestion, discrepancies will occur due to bank fee variances, FX fluctuations, human input errors in purchase orders, and payment gateway settlement adjustments. The CFO OS manages these exceptions using autonomous parser agents.

These agents run continuously, monitoring ledger inputs. When a discrepancy is detected, the agent analyzes the transaction history, matches receipts, checks contract agreements, and resolves the issue automatically, or builds a structured ticket for human review.

Below is an implementation of a transactional discrepancy check agent. The script parses transaction feeds, compares them against ERP invoices, handles foreign currency conversion checks, and logs discrepancy flags with structured metadata.

import re

from datetime import datetime

from typing import Dict, List, Optional

class FinancialTransaction:

def __init__(self, tx_id: str, amount: float, currency: str, timestamp: datetime, description: str):

self.tx_id = tx_id

self.amount = amount

self.currency = currency

self.timestamp = timestamp

self.description = description

class ERPInvoice:

def __init__(self, invoice_id: str, expected_amount: float, currency: str, status: str):

self.invoice_id = invoice_id

self.expected_amount = expected_amount

self.currency = currency

self.status = status

class AuditDiscrepancy:

def __init__(self, tx_id: str, invoice_id: str, code: str, severity: str, details: str):

self.tx_id = tx_id

self.invoice_id = invoice_id

self.code = code # FX_MISMATCH, AMOUNT_MISMATCH, FEE_VARIANCE

self.severity = severity # LOW, MEDIUM, CRITICAL

self.details = details

class DiscrepancyParserAgent:

def __init__(self, fx_rates: Dict[str, float], variance_tolerance: float = 0.02):

self.fx_rates = fx_rates

self.variance_tolerance = variance_tolerance

def parse_invoice_ref(self, description: str) -> Optional[str]:

# Extract invoice reference codes (e.g. INV-2026-9081)

match = re.search(r"INV-\d{4}-\d+", description, re.IGNORECASE)

return match.group(0).upper() if match else None

def convert_currency(self, amount: float, from_curr: str, to_curr: str) -> float:

if from_curr == to_curr:

return amount

rate_from = self.fx_rates.get(from_curr.upper(), 1.0)

rate_to = self.fx_rates.get(to_curr.upper(), 1.0)

# Convert to base currency then to target currency

base_amount = amount / rate_from

return round(base_amount * rate_to, 2)

def reconcile_transaction(self, tx: FinancialTransaction, invoice: ERPInvoice) -> Optional[AuditDiscrepancy]:

# Convert invoice amount to transaction currency for direct comparison

converted_expected = self.convert_currency(

invoice.expected_amount, invoice.currency, tx.currency

)

diff = abs(tx.amount - converted_expected)

if diff == 0:

return None # Perfect match

# Check if the discrepancy is within standard tolerance threshold

if diff <= self.variance_tolerance:

return AuditDiscrepancy(

tx_id=tx.tx_id,

invoice_id=invoice.invoice_id,

code="TOLERABLE_VARIANCE",

severity="LOW",

details=f"Minor variance of {tx.currency} {diff:.2f} within threshold."

)

# Check if difference matches typical bank transfer fee patterns

if 5.0 <= diff <= 45.0 and tx.currency == "USD":

return AuditDiscrepancy(

tx_id=tx.tx_id,

invoice_id=invoice.invoice_id,

code="BANK_FEE_VARIANCE",

severity="MEDIUM",

details=f"Variance of {tx.currency} {diff:.2f} matches standard bank wiring fees."

)

# Check for currency exchange rate discrepancies

if invoice.currency != tx.currency:

return AuditDiscrepancy(

tx_id=tx.tx_id,

invoice_id=invoice.invoice_id,

code="FX_RATE_MISMATCH",

severity="HIGH",

details=f"Significant FX variance. Expected {tx.currency} {converted_expected:.2f}, got {tx.currency} {tx.amount:.2f}."

)

return AuditDiscrepancy(

tx_id=tx.tx_id,

invoice_id=invoice.invoice_id,

code="UNRESOLVED_DISCREPANCY",

severity="CRITICAL",

details=f"Unexplained mismatch of {tx.currency} {diff:.2f} between transaction and invoice."

)

# Example execution dataset

if __name__ == "__main__":

rates = {"USD": 1.0, "EUR": 0.92, "GBP": 0.78}

agent = DiscrepancyParserAgent(fx_rates=rates)

test_tx = FinancialTransaction(

tx_id="TXN_809123",

amount=1025.40,

currency="EUR",

timestamp=datetime.utcnow(),

description="Wire transfer payment for invoice INV-2026-4412"

)

# ERP invoice expects $1150 USD

test_invoice = ERPInvoice(

invoice_id="INV-2026-4412",

expected_amount=1150.00,

currency="USD",

status="UNPAID"

)

discrepancy = agent.reconcile_transaction(test_tx, test_invoice)

if discrepancy:

print(f"[{discrepancy.severity}] Flagged {discrepancy.code}: {discrepancy.details}")

else:

print("Transaction reconciled successfully with zero errors.")By deploying this logic at the transaction gateway, the system isolates accounting errors immediately. Instead of waiting for month-end reconciliation scripts to fail, the discrepancy parser agent flags mismatch items the day they occur, alerting treasurers to address the issue before it propagates through consolidated statements.

The parser agents operate on a stateful, event-driven pattern. When a transaction is flagged, the agent does not simply raise an alert; it initiates a local investigative workflow. It queries external APIs (such as shipping provider tracking logs to confirm delivery dates, or vendor contract management databases to check for pre-negotiated discounts) to see if the variance can be explained. If the agent resolves the discrepancy, it automatically posts an adjusting entry with the supporting evidence attached, reducing manual audit burdens.

Stateful Agent Auditing Workflows: From Identification to Journal Correction

When a discrepancy is identified, the parser agent executes a structured resolution sequence to minimize manual corrections:

- Analyze Transaction Context: The agent reads metadata associated with the flag, identifying if the mismatch matches standard bank fees, currency rounding errors, or tax withholding patterns.

- Verify External Sources: The agent queries vendor systems or shipping logs (such as DHL or FedEx APIs) to cross-reference actual delivery dates and payment requirements.

- Draft Adjusting Entries: If a known pattern is matched (e.g. a wire transfer fee of $15 USD), the agent drafts an adjusting entry to post the difference to a bank charges expense account.

- Validate Compliance Constraints: The draft entry is passed to compliance check filters to ensure that internal controls (such as Sarbanes-Oxley or corporate treasury policies) are satisfied.

- Commit Adjustment: If all controls pass, the agent commits the journal correction to the ledger database, linking the supporting API payloads as audit evidence.

This automated correction workflow ensures that simple, routine reconciliation issues are handled without manual human intervention, freeing up controllers to focus on complex audit exceptions.

Exception Resolution and Escalation Protocols

If a discrepancy cannot be matched to a known pattern or exceeds acceptable threshold levels (such as an unexplained mismatch of $5,000 USD on a supplier invoice), the agent initiates an escalation protocol:

- Hold Ledger Account: The transaction status is marked as

UNRESOLVEDand placed in a dedicated audit exception table. - Block Duplicate Payments: The system automatically holds any subsequent payment cycles related to the affected purchase order to prevent duplicate payouts.

- Generate Compliance Alert: A notification is sent to the designated controller, containing the transaction payload, matching invoices, and the agent's research log.

- Initiate Collaborative Review: The controller can review the discrepancy details, adjust ledger records, or request additional invoice details from the vendor directly through the finance dashboard.

By isolating exceptions and preventing automated balance sheets updates on uncertain data, the escalation protocol preserves ledger integrity and prevents compliance issues.

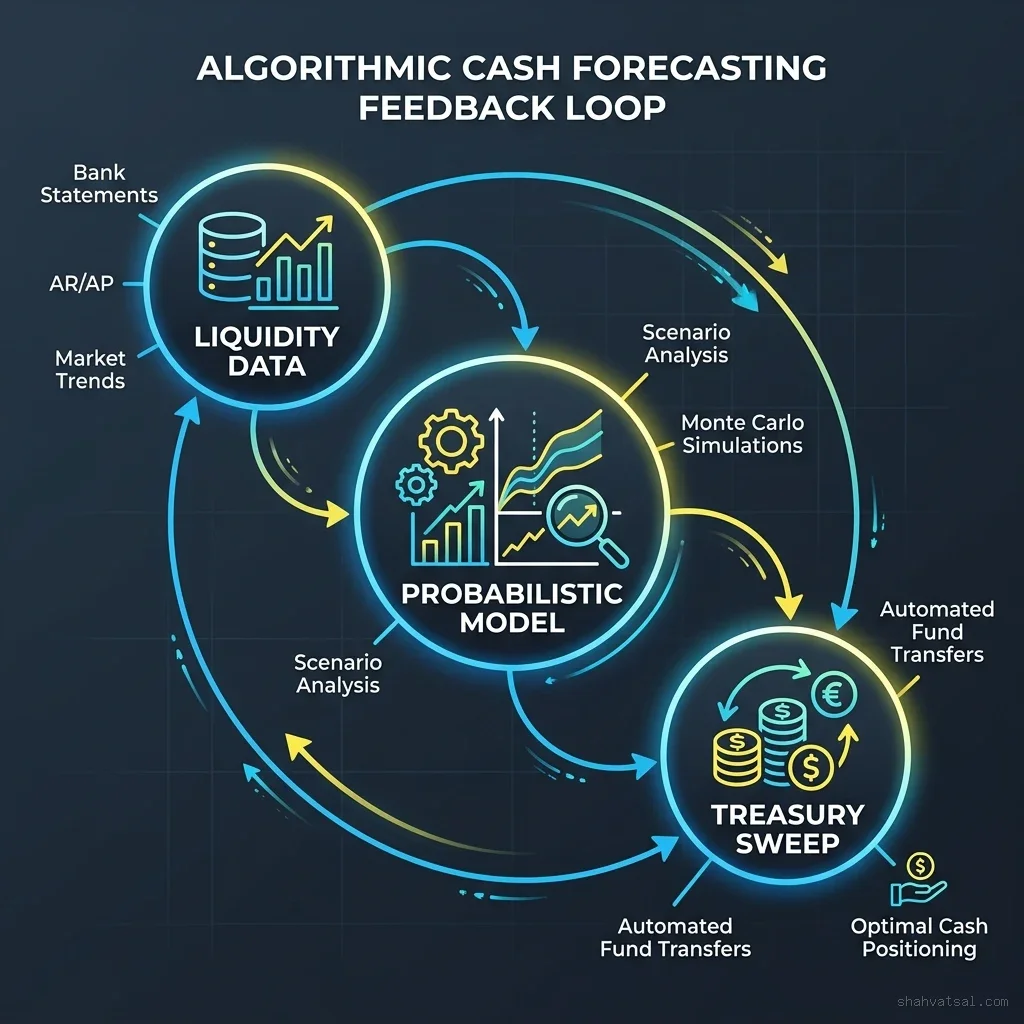

Predictive Liquidity: Modeling Mid-Term Operational Working Capital Needs

Reconciliation is only the first step. To drive strategic business value, the CFO OS leverages real-time transaction data to model predictive liquidity. Traditional treasury relies on cash projections based on manual spreadsheets. This static process fails to account for payment delays, dynamic supply chain disruptions, or shifting vendor payment terms.

An autonomous finance stack uses predictive models to dynamically adjust working capital requirements.

We calculate the Composite Liquidity Score ($L_c$) for any given operational window using the following model:

$$L_c = \frac{C_t + \sum (AR_i \times P_i) - \sum (AP_j \times V_j)}{W_{req}}$$

Where:

- $C_t$: Immediate cash equivalents at time $t$ across all verified treasury accounts.

- $AR_i$: The value of outstanding accounts receivable invoice $i$.

- $P_i$: The probability of payment for receivable invoice $i$, modeled dynamically using historical client payment latency distributions. Instead of assuming standard Net-30 payment terms, $P_i$ is calculated as a probability density function based on the client's past payment behaviors and industry payment indices.

- $AP_j$: The value of outstanding accounts payable invoice $j$.

- $V_j$: The vendor payment flexibility coefficient (how late a payment can be deferred without incurring penalties or damaging relationship indexes).

- $W_{req}$: Dynamic operational working capital requirements based on moving averages of operational expenses, factoring in payroll schedules, tax liabilities, and recurring infrastructure costs.

Citation Anchor: AI-Driven Working Capital Optimization

Financial operations audits from institutions like McKinsey show that transitioning from deterministic cash models to probabilistic working capital models reduces safety cash requirements by 18% to 25%. This optimization allows corporate treasurers to redeploy idle balances into short-term cash instruments or strategic capital investments.

Calculating $L_c$ continuously changes how enterprises manage treasury operations. Instead of holding large cash buffers to cover potential accounts receivable delays, treasurers use real-time cash forecasting loops to target precise cash requirements.

For example, if the system models a payment probability $P_i$ for a major client that drops due to industry factors, it immediately raises the required cash buffer, preventing overdrafts. Conversely, when payment probabilities are high, the treasury system can safely deploy capital into high-yield, short-term instruments, capturing incremental revenue that would otherwise be lost in static operating accounts.

This modeling capability extends to automated cash sweeps. When $L_c$ exceeds a pre-defined threshold, the CFO OS triggers capital allocation APIs to sweep the surplus cash into a diversified yielding portfolio. If the score falls, the system automatically draws down on pre-negotiated revolving credit lines, ensuring operational continuity without manual intervention from treasury staff.

Deep-Dive: Formulating Client Payment Latency Probability Distributions

To calculate $P_i$ accurately, the system builds client-specific payment profiles. In legacy accounting, accounts receivable teams rely on generic metrics like Days Sales Outstanding (DSO) to estimate when cash will clear. DSO, however, is a retrospective average that fails to capture changes in client behavior or macroeconomic volatility.

The CFO OS models payment latency ($T_L$) as a random variable using a log-normal probability density function:

$$f(t; \mu, \sigma) = \frac{1}{t\sigma\sqrt{2\pi}} \exp\left( -\frac{(\ln t - \mu)^2}{2\sigma^2} \right), \quad t > 0$$

Where:

- $t$: The number of days elapsed past invoice issuance.

- $\mu$: The historical location parameter of invoice settlement for a specific client profile.

- $\sigma$: The scale parameter representing payment variance under different seasonal or interest-rate environments.

Using this model, the system calculates $P_i(t_{target})$, which represents the probability that outstanding invoice $i$ will be settled by date $t_{target}$. If the client has historically paid between day 12 and 15, the probability curve shows a narrow variance, letting the treasury team project exact cash arrivals. If the client has a history of erratic payments, the variance scale ($\sigma$) widens, signaling the cash allocation system to hold a larger buffer to offset collection uncertainty.

Automating Treasury Sweeps and Revolving Credit Lines Using Dynamic Liquidity Buffers

When the system calculates a high Composite Liquidity Score ($L_c$), it signals the treasury engine that the corporation possesses surplus cash. This surplus represents an opportunity cost if left idle in operating bank accounts that earn zero interest.

The CFO OS automates the capital deployment cycle using programmable cash sweep rules:

- Monitor Balance Thresholds: If $L_c$ remains above $1.5$ for three consecutive business days, the system identifies the surplus capital volume ($C_{surplus}$).

- Determine Allocation Strategy: Based on pre-set corporate investment policy rules, the cash sweep service partitions $C_{surplus}$ into conservative, high-liquidity assets (such as overnight commercial paper or short-term Treasury bills).

- Execute Transfer: The sweep engine initiates API-driven bank transfers to move the funds to the yield-bearing investment accounts.

- Automated Recall: If a sudden surge in Accounts Payable (AP) occurs or a major client defaults, causing $L_c$ to drop below $1.0$, the engine automatically sells the short-term assets and recalls the cash to the primary operating accounts.

By automating this cycle, the enterprise captures incremental yields while maintaining complete liquidity security, reducing the time controllers spend managing treasury allocations.

Legacy Periodic vs. Autonomous CFO OS

Transitioning from traditional accounting to the CFO OS requires replacing old batch structures with modern streaming equivalents.

| Dimension | Legacy Periodic Accounting | Autonomous CFO OS |

|---|---|---|

| Data Ingestion | Monthly manual downloads or nightly batch files (BAI2/MT940). | Real-time Webhook-driven bank API integration. |

| Reconciliation | Manual spreadsheet matching or rule-based matching run once a month. | Continuous automated matching with fuzzy heuristics and parser agents. |

| Error Detection | Discovered retrospective-style weeks after occurrence. | Flagged in real time with automated notification to treasurers. |

| Liquidity Forecasting | Static spreadsheet projections based on historical assumptions. | Dynamic probabilistic modeling of receivable latency ($P_i$). |

| Audit Readiness | High stress periods with substantial manual forensic labor. | Continuous audit posture with verified, clean ledgers. |

Pitfalls and Modern Anti-Patterns

Implementing a continuous close architecture requires avoiding several key mistakes:

Anti-Pattern 1: Webhook Ingestion Without Event Validation and Idempotency

Relying on direct bank webhook APIs is critical for streaming accounting, but ingesting these events without robust security and processing validation introduces severe vulnerabilities:

- Security Vulnerability: Bank webhook endpoints are exposed to the public internet. If an attacker discovers the endpoint URL, they can send falsified JSON payloads, creating fake cash deposits or adjusting invoice statuses to commit balance sheet fraud.

- Ledger Corruption: Network interruptions often cause webhooks to be delivered out of sequence or retried multiple times. If the ingestion pipeline does not enforce message idempotency, the ledger database will process the same transaction repeatedly, corrupting balances.

To avoid this, all webhook endpoints must validate cryptographic signatures (such as HMAC tokens with SHA256) and reject duplicate message IDs using unique database keys.

Anti-Pattern 2: Alert Fatigue from Zero-Variance Match Rigidness

When designing matching logic rules, a common mistake is requiring absolute precision on every transaction validation vector. In the real world, minor variances are standard:

- Cent-level discrepancies occur regularly due to differences in currency exchange rounding formulas between banks.

- Merchant gateway fees are often deducted directly from customer payments, causing transaction amounts to fall short of invoice values by minor percentage amounts.

If the matching system flags every micro-variance, accounts receivable queues will flood with minor flags, causing alert fatigue. To prevent this, the engine must use dynamic variance tolerance thresholds, allowing minor deviations to reconcile automatically to designated fee accounts.

Anti-Pattern 3: Stale FX Reference Data on International Cross-Border Ledger Reconciliation

Organizations with international operations often make payments in multiple currencies. A common anti-pattern is using a static monthly exchange rate (or a daily rate updated only in the morning) to reconcile transactions:

- The Valuation Gap: Exchange rates fluctuate throughout the day. If a high-value payment is reconciled using a morning rate while the transaction cleared in the afternoon, the mismatch can generate false discrepancy alerts or mask actual bank fee overcharges.

- Compliance Liabilities: Retrospective audit standards demand that currency transactions represent actual spot values at settlement time. Using stale exchange rates introduces audit reporting compliance risks.

The matching engine must query live, timestamped spot FX rates at transaction execution time to ensure ledger conversions reflect financial reality.

Anti-Pattern 4: Balance Sheet Pooling Without Inter-Company Entity Segregation

In corporate group structures, parent organizations often pool cash from subsidiary accounts into a single treasury account to maximize interest yield. While cash pooling is highly efficient, automated sweeps can complicate tax accounting if inter-company balances are not tracked:

- Tax Audit Risk: Tax authorities require inter-company fund transfers to carry appropriate transfer pricing interest rates and be logged as explicit loans. If the system sweeps cash automatically without creating matching parent-subsidiary debt entries, it generates tax audit liabilities.

- Liquidity Tracking Failure: Cash pooling without inter-company entity segregation makes it impossible to assess the individual solvency of local subsidiaries, hiding operational underperformance.

To prevent this, the cash sweep logic must write offsetting debit and credit entries to inter-company loan ledger accounts for every automated bank transfer.

Futuristic Horizon: 2027–2030 Roadmap

Over the next few years, the role of corporate finance will shift from record-keeping to autonomous treasury optimization.

2026: Webhook Ingestion & Automated Matchers -> 2028: Multi-Agent Consensus Auditing -> 2030: Zero-Day Close & Autonomous Capital Reinvestment- 2026–2027: Standardization of open corporate bank APIs globally. Widespread adoption of discrepancy parser agents and edge reconciliation. Enterprises deprecate legacy MT940 text-based batch file imports.

- 2028–2029: Multi-agent consensus protocols. Autonomous agents representing vendors, banks, and buyers verify transactions against shared cryptographic ledgers, eliminating traditional bank reconciliation loops.

- 2030 and Beyond: Zero-day close. Consolidated financial books are maintained in a continuous audit state, enabling real-time tax filing, dynamic dividend distributions, and autonomous treasury reallocation.

Key Takeaways

- Obsolete Close Loop: Waiting 30 days to consolidate ledger books hinders corporate agility and leaves companies exposed to fraud and liquidity constraints.

- Continuous Ingestion: Reconciling cash at the edge requires Webhook-driven bank APIs, normalization pipelines, and transactional deduplication keys.

- Heuristic Agent Matching: Parser agents must handle currency conversions and bank fees flexibly to resolve issues automatically, minimizing human overhead.

- Dynamic Capital Optimization: Probabilistic liquidity scores, using client-specific payment patterns, allow treasury systems to minimize idle cash securely.

- Continuous Audit Posture: Transitioning to the CFO OS creates a continuous audit-ready state, reducing compliance stress and forensic costs.

What to Do Monday Morning

To start building a continuous close architecture:

- Audit Bank Connectivity: Catalog all active corporate accounts and identify which banks provide transaction APIs (Plaid, Stripe, or direct webhook systems) to replace file-based MT940 batch processing.

- Map Matching Logic: Document manual ledger reconciliation steps to establish matching rules (exact invoices, purchase orders, expected fees, and FX rates) for automation scripts.

- Deploy a Transaction Tracker: Build a containerized parser script (such as the Python reconciliation agent above) to match incoming transactions against open ERP invoices in a test sandbox environment.

FAQ

How does the CFO OS handle transactions with multiple matching candidates?

When the parser agent identifies multiple potential matches (e.g. two open invoices for the same customer with the same amount), it uses metadata heuristics to resolve the ambiguity. It checks purchase order numbers, payment timestamps, and email invoice details. If the ambiguity remains, the agent places the transaction in a temporary hold queue and escalates it to a human treasurer with the matching choices highlighted.

Is real-time reconciliation secure against external manipulation?

Yes, security is built-in. Every transaction ingested via bank API endpoints must be signed using cryptographic signatures (such as HMAC tokens with SHA256) and verified against bank public certificates. Ledgers are maintained on write-once, read-many databases to ensure audit changes are appended rather than overwritten, maintaining data integrity.

How do currency exchange fluctuations affect continuous auditing?

The CFO OS retrieves real-time currency exchange rates from authorized API providers (like OANDA or Open Exchange Rates) at the timestamp of transaction execution. The discrepancy parser agent uses this historical rate to convert expected invoice balances to transaction currency, matching variances within tolerable limits without generating false mismatch flags.

Can this architecture integrate with legacy ERP platforms like SAP or Oracle?

Yes. The CFO OS acts as an orchestration layer between transactional gateways and legacy ERPs. It ingests bank API feeds at the edge, normalizes them, runs the matching logic, and updates SAP or Oracle via standard REST APIs, SOAP endpoints, or scheduled batch uploads, allowing enterprises to keep their core system of record.

What are the direct compliance benefits of a continuous close?

Continuous reconciliation maintains books in a pre-audited state, drastically reducing year-end audit timelines and costs. It helps prevent SOX compliance violations by implementing automated check controls that immediately flag duplicate payments, unauthorized asset withdrawals, and ledger tampering.

About the Author

Vatsal Shah is a technology executive and systems architect specializing in enterprise AI integrations, FinOps infrastructure, and data platforms. He helps global enterprises modernize legacy systems, automate complex financial processes, and optimize unit economics through strategic technology deployments.